USDT Insolvent? Arthur Hayes Publicly Questions Tether

Original Title: "Arthur Hayes Warns of USDT Insolvency Risk, Why the Recent FUD Frenzy?"

Original Author: Azuma, Odaily Star Daily

Following a public feud with Monad, "Big Brother" Arthur Hayes has once again unexpectedly clashed with the stablecoin king Tether.

Arthur Hayes: USDT May Face "Insolvency" Risk

The incident originated on November 30th when Arthur Hayes posted on X regarding Tether's publicly disclosed third-quarter reserves at the end of October. He analyzed that Tether's allocation of volatile assets such as gold and Bitcoin in its reserve assets is too high. USDT may face an "insolvency" risk due to the decline of these assets.

"The Tether team is in the early stages of a massive interest rate trade. Based on my understanding of their audit report, they believe the Fed will start cutting rates, which will significantly compress their interest income. In response, they started buying gold and Bitcoin—ideally, when the 'currency price falls' (rate cut), these assets should rise. But if their gold + Bitcoin position drops by about 30%, Tether's equity will be wiped out, and USDT theoretically will face insolvency."

As shown in the above chart, out of a total of $181.223 billion in Tether's reserve assets, there is a $12.921 billion reserve of precious metals (7.1% share) and a $9.856 billion reserve of Bitcoin (5.4% share)—the combined share of these two assets reaches 12.5% of Tether's total reserve assets.

From Tether's reserve structure, it can be seen that Arthur Hayes may have objectively pointed out a potential extreme scenario that Tether may face. If the gold and Bitcoin reserves simultaneously experience a significant devaluation, theoretically, the value of Tether's reserve assets will not be able to fully cover the issuance scale of USDT.

This point was also mentioned by the well-known rating agency Standard & Poor's last week when downgrading Tether's and USDT's stability ratings, stating "Tether's Bitcoin reserve value accounts for approximately 5.6% of the total USDT circulation volume (Odaily Note: Standard & Poor's here is comparing circulation volume, so the percentage data will be slightly higher than when compared to reserves), exceeding USDT's own 3.9% excess collateralization rate. This means that other low-risk reserve assets (mainly government bonds) are no longer able to fully support the value of USDT. If BTC and other high-risk assets decline in value, it may weaken the coverage ability of USDT's reserves, leading to under-collateralization of USDT."

Is USDT Still Safe?

Arthur Hayes actually described the same situation as Standard & Poor's, but the likelihood of this situation actually occurring is very minimal, for two specific reasons.

· Firstly, it is hard to imagine an instantaneous sharp drop in the price of gold and Bitcoin (referring to a drop of at least several tens of points in a very short period), even in a scenario of sustained decline, Tether theoretically has time to replenish its reserve of low-risk assets by selling.

· Secondly, besides its reserve assets, Tether itself holds a huge amount of proprietary assets, which are sufficient as a reserve buffer pool for USDT to sustain the operation of this cash flow machine.

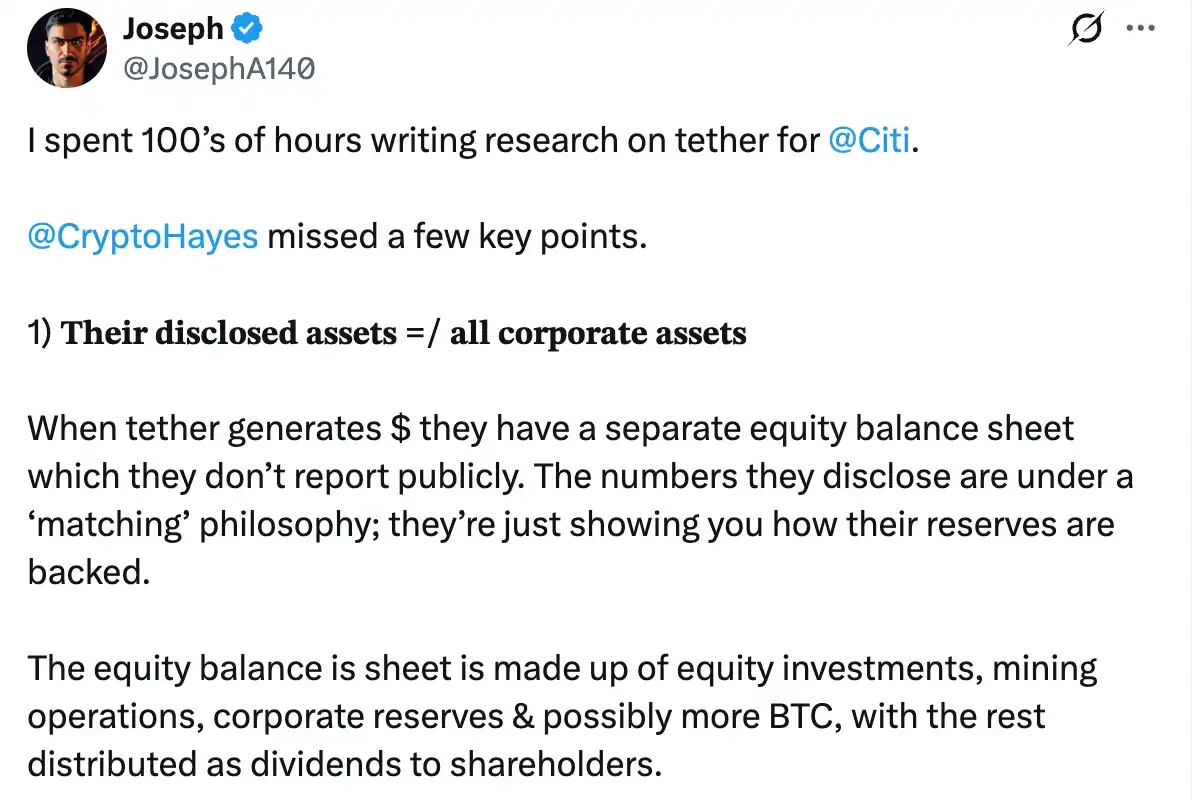

Joseph, former Cryptocurrency Research Head at Citigroup, also mentioned the second point, stating that the assets disclosed by Tether do not represent all of its holdings—when Tether generates profits, they have a separate equity balance sheet that is not publicly disclosed together with the reserve situation; Tether has an extremely strong profitability, and the value of its equity is very high, allowing them to offset any gaps on the balance sheet by selling equity; Tether will not go bankrupt; on the contrary, they have a money-printing machine.

Tether's Response

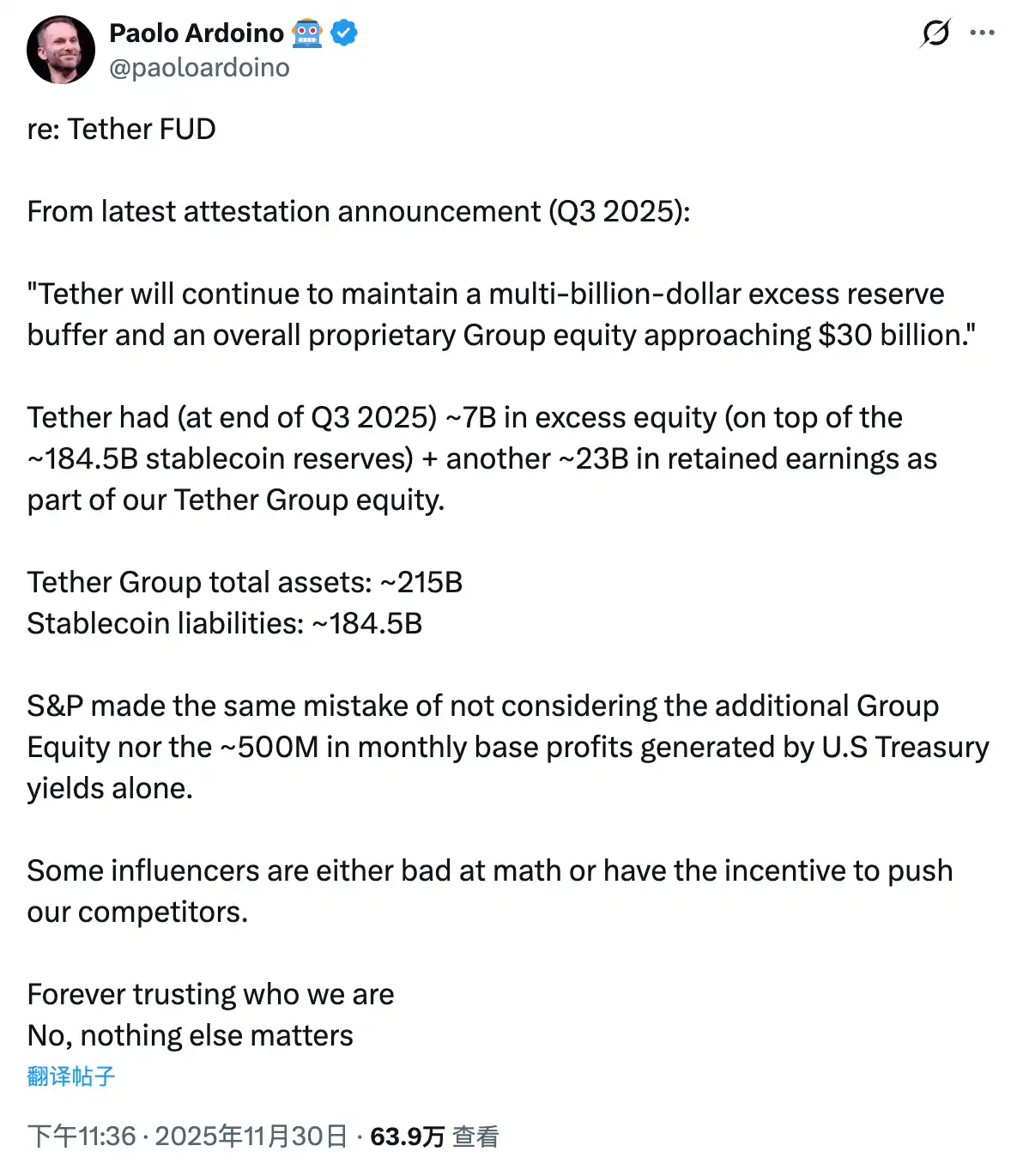

Yesterday evening, as FUD related to this matter escalated, Tether's CEO Paolo Ardoino responded in a post, stating that as of the end of the third quarter of 2025, Tether holds approximately $70 billion in excess equity (beyond the approximately $184.5 billion stablecoin reserves), along with an additional approximately $23 billion in retained earnings, together constituting Tether Group's proprietary equity.

A clear comparison of assets and liabilities:

· Total assets of the Tether Group: approximately $215 billion;

· Stablecoin liabilities: approximately $184.5 billion;

Standard & Poor's also made the same mistake, failing to account for these additional group equities, and not considering the approximately $500 million in basic monthly profits generated solely from U.S. Treasury bond returns.

Interestingly, Paolo Ardoino concluded with a special note: "Some internet celebrities either have poor math skills or impure motives."

· Odaily Note: Arthur Hayes and his family office investment firm Maelstrom are key investors in the interest-bearing stablecoin Ethena (USDe), and have repeatedly predicted that USDe will become the largest stablecoin by issuance volume.

After Paolo Ardoino responded directly, Arthur Hayes also replied again, but his remarks were somewhat sarcastic: "You guys are making so much money, I'm so jealous. Do you have a specific dividend policy? Or a target overcollateralization rate based on asset type (discounted by its volatility)? Obviously, when your liability is in dollars and your asset is U.S. Treasuries, there is no problem, but if your asset is illiquid private investments, in case of an accident, people may question your claim of being overcollateralized."

After this exchange, neither party continued to reply. Arthur Hayes did post a dynamic this morning, but it was just about calling a bounce in the market.

From the photos shared by Arthur Hayes, after ranting about Monad and Tether in succession, his mood seemed quite good...

You may also like

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.